Tell us what you are building, where your payment flow gets complex, or what is slowing rollout down. We will come back to you with the next best step.

Why Are Cross-Border Payments Still Slow, Expensive, and Unpredictable in 2026?

Cross-border payments are slow, expensive, and unpredictable because the transfer is only one part of the system. The real complexity sits in FX, compliance, local payout rails, reconciliation, provider statuses, retries, and auditability. Stablecoins can improve settlement, but infrastructure determines whether the flow is usable in production.

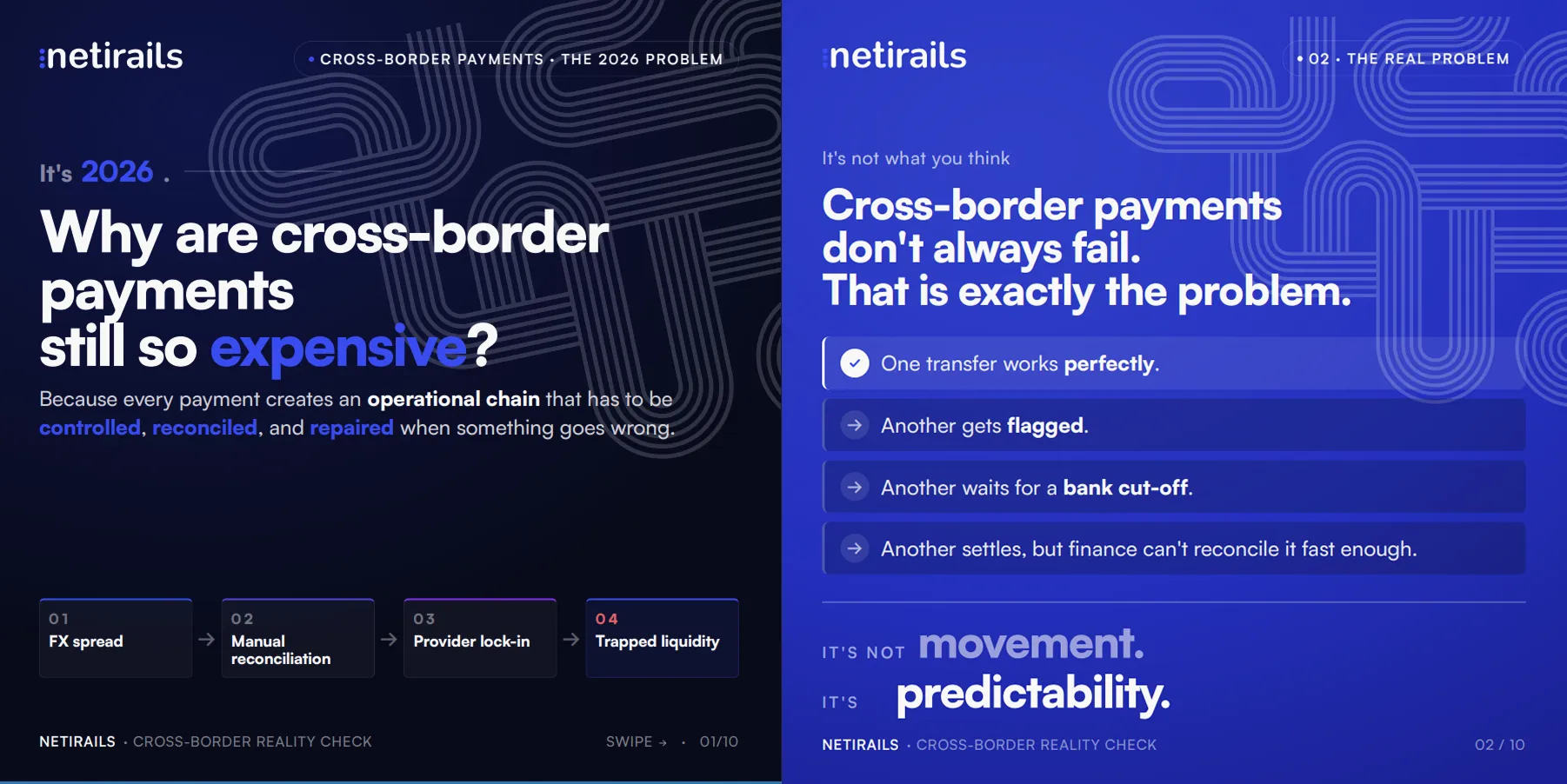

Most teams learn cross-border payments the expensive way: by assuming the hard part is moving money. Usually, it isn’t. Cross-border payments do not always collapse. They get delayed, flagged, reviewed, rerouted, settled later than expected, converted at a worse rate than planned, and matched manually by someone in finance three days after everyone thought the payment was done. That is the main problem. The worst part of cross-border payments is not always the cost. It is the uncertainty.

One transfer goes through smoothly. Another gets stuck for additional checks. A third depends on bank cut-off times. A fourth arrives, but the internal ledger, provider report, and bank statement do not agree fast enough for finance to close the loop.

For an individual, this is frustrating. For a business paying suppliers, contractors, vendors, or partners across markets, it becomes an operating risk.

Stablecoins look like the obvious fix. They move fast, settle 24/7, reduce dependency on correspondent banking, and can make liquidity more efficient.

The numbers are already absurd. Visa’s stablecoin data counted $47 trillion in raw on-chain stablecoin transaction volume, but only $10.4 trillion after adjusting for high-frequency trading and other non-payment activity. That gap is the whole story: stablecoins can move value at massive scale, but moving value is not the same as running a reliable payment system.

So why has this not been solved already? Because cross-border payments are not just about moving money. They are about trust, compliance, FX, local rails, reconciliation, support, and what happens when the happy path breaks.

The rail can be modern but the operating model can still be a mess.

In short: Cross-border payments are slow, expensive, and unpredictable because the transfer is only one part of the system. The real complexity sits in FX, compliance, local payout rails, reconciliation, provider statuses, retries, and auditability. Stablecoins can improve settlement, but infrastructure determines whether the flow is usable in production.

What are cross-border payments and how do they work?

Cross-border payments are financial transactions between people, businesses or institutions located in different countries. They are used for supplier payments, contractor payouts, remittances, marketplace payouts, treasury transfers and financial settlement, usually involving currency conversion, compliance checks, payment providers, local rails and settlement systems.

Simple definition. Messy reality.

To the customer, it looks like one payment.

To the company operating the flow, it is a multi-system workflow where money, FX, compliance, banking rails, local payout providers, ledgers, statuses, exceptions, reconciliation, audit trails, and customer expectations all have to agree on what happened.

Spoiler: they often don’t.

That is why cross-border payments are used for many different flows:

B2B supplier payments,

international contractor payouts,

marketplace payouts,

remittances,

vendor payments,

treasury transfers,

settlement between financial institutions.

The clean version is: money moves between countries.

The useful version is: money moves between countries through systems that were not built to behave like one system.

That is where the trouble starts.

Cross-border payments remain more costly, slower, less accessible, and less transparent than domestic payments, despite progress in domestic payment systems. BIS points to limited interoperability as one of the core constraints.

In other words: this is not just a payment method.

It is an infrastructure problem with a payment screen on top.

Simple view

Operating reality

Money moves between countries

Multiple systems must agree on what happened

One payment status

Banks, PSPs, ledgers, FX providers and payout partners may show different statuses

One visible fee

FX spread, prefunding, reconciliation and failed payment handling add hidden cost

Payment completed

Payment must still be reconciled, audited and explained

Why cross-border payments are not broken, but inconsistent

Saying “cross-border payments are broken” is too easy. It is also not quite true. Sometimes they work exactly as expected.

A fintech sends a supplier payment through its usual provider and it clears on time. No issue. A payout ops team sends contractor payments across one corridor and everything reconciles cleanly. No escalation. A finance team uses a bank rail, PSP, FX provider, or payout partner and the flow behaves exactly as expected. No reason to question the setup.

Then the next payment behaves differently. It gets flagged. Or delayed. Or converted at a worse rate than expected. Or held for additional documentation.

Or marked as “processed” by one provider while another system still thinks it is pending.

That is what makes the problem hard to manage.

Cross-border payments work often enough to look reliable, but not consistently enough to build serious operations around them.

For one-off payments, that is manageable.

For fintechs, neobanks, payment institutions, and finance teams running supplier payments, contractor payouts, marketplace settlements, or treasury flows across corridors, it becomes a control problem.

The question is not:

Can this payment go through?

The better question is:

Can this payment flow behave predictably when volume, corridors, providers, compliance checks, retries, and edge cases start piling up?

A successful transfer proves the happy path works.

It does not prove the operating model works.

And in cross-border payments, the operating model is where things usually get expensive.

Why are cross-border payments still expensive?

Cross-border payments are expensive because the visible transaction fee is only one part of the total cost.

A business may see a wire fee, card processing fee, or payout fee first. But the real cost often sits across the full payment flow: FX spread, currency conversion markup, correspondent banking deductions, receiving bank charges, prefunded liquidity, settlement delays, failed payment handling, and manual reconciliation.

That is why cross-border payment cost is easy to underestimate. The fee is visible. The leakage is distributed.

For example, a business selling into another currency market may pay the card processor, then pay for currency conversion, then absorb a bank FX spread, then spend finance time reconciling payment records across processor reports, bank statements, and internal ledger entries.

No single line item looks catastrophic.

Together, they can turn cross-border growth into margin compression.

For B2B payments, the same issue becomes even more operational.

If a company keeps liquidity parked across markets to make payouts predictable, that capital has a cost.

If finance teams need to manually match provider reports, bank statements, ledger entries, FX records, and payout statuses, that work also has a cost.

It may not appear as a payment fee.

But it still reduces margin.

This is why cross-border payment infrastructure should be evaluated on total operating cost, not only transaction pricing.

Why cross-border B2B payments are harder to operate at scale

Cross-border B2B payments are harder than consumer transfers because the payment is rarely the end of the process.

A business payment has to be approved, screened, converted, routed, settled, recorded, reconciled, reported, and explained later. It may involve an invoice, a supplier record, a contract, a payout file, an internal ledger, an FX quote, a compliance decision, and a finance close process. That means a successful transfer is not enough. One corridor can be handled manually. Ten corridors create status mismatches, local payout differences, FX complexity, liquidity buffers, provider-specific reports, and exceptions that live in Slack, inboxes, spreadsheets, and back-office workarounds.

That is why cross-border B2B payments need more than a faster rail. They need a controlled operating layer around the payment flow: normalized statuses, exception handling, safe retries, ledger consistency, reconciliation-ready data, and an audit trail that shows what happened from start to finish.

Without that layer, every new provider, corridor, currency, and compliance requirement adds operational debt.

With that layer, cross-border B2B payments become easier to scale without turning finance and operations into a manual control system.

The future of cross-border payments is orchestration, not one perfect rail

There will not be one magic rail for all cross-border payments.

Some payments will still move through banks. Some through fintech providers. Some through stablecoin rails. Some will need local payout partners because the last mile is where the nice architecture diagram usually gets humbled.

FX providers will still matter. Compliance providers will still matter. Custody providers will still matter. The future is not one rail replacing everything. The future is making several rails, providers, currencies, checks, statuses, and failure scenarios behave like one controlled payment flow.

That is orchestration.

A serious cross-border payment system needs to coordinate the full lifecycle without forcing the business to rebuild the payment core every time a corridor, provider, currency, or compliance requirement changes.

That is where architecture becomes strategy.

If every provider is hardcoded into the core business logic, each new corridor becomes a rebuild.

If retries are not idempotent, failed flows can create duplicate payments or broken financial state.

If compliance decisions are not captured in the workflow, auditability breaks.

If the ledger does not reflect reservations, debits, credits, fees, and settlement states correctly, finance will not trust the system.

This is why payment orchestration is not just a technical pattern.

It is how businesses avoid turning payment operations into a permanent exception-handling department.

Planning a cross-border stablecoin payment flow?

Start with one corridor, one B2B scenario and one operating model for statuses, exceptions, retries and reconciliation. NetiRails helps payment teams validate whether their flow is ready for production, before the provider stack becomes expensive to change.

Where NetiRails fits in cross-border payment infrastructure

This is where NetiRails comes in. Not as another payment app or as another crypto experiment. Not as “give us developers and we’ll figure it out.” NetiRails is built for fintechs, payment institutions, neobanks, and product teams that want to launch cross-border stablecoin payments without turning the project into a never-ending infrastructure build. The job is not to prove that stablecoins can move value. They can. The real job is making stablecoin payments usable in production: controlled, auditable, compliance-ready, and reliable enough for real payment operations. That means the business needs to answer the boring questions that decide whether a payment flow can actually go live:

Where is the payment?

Why is it in this status?

Can it be retried safely?

Did compliance approve it before funds moved?

Does the ledger reflect the real financial state?

Can finance reconcile the flow?

Can an auditor reconstruct what happened?

Can a new provider or corridor be added without rebuilding the core?

That is the layer NetiRails is built for. NetiRails is a delivery partner for cross-border stablecoin payments. The goal is not to sell a technology stack or extra development capacity. The goal is to deliver a working payment capability: one controlled B2B flow, with statuses, exceptions, retries, reconciliation, operations, and audit trail designed into the system from the start.

Under the hood, NetiRails coordinates the components that usually make stablecoin payment projects messy: wallet and custody, ledger, FX, KYC/KYT, on-ramp, off-ramp, payment statuses, retries, reconciliation, audit trail, and provider changes.

Its architecture uses canonical internal models, typed mediator interfaces, and durable workflow execution to make fragmented providers behave like one controlled payment flow. Every third-party provider category - Ledger, Wallet, FX, KYC, Ramp - is abstracted behind a typed mediator, so providers can be changed without touching the core business logic.

That detail matters. Because in cross-border payments, provider replaceability is not an engineering nice-to-have. It is how you reduce vendor lock-in. It is how you add corridors without rebuilding the payment core. It is how you keep reconciliation, compliance, and financial state under control when different systems produce different statuses, timings, and failure modes.

NetiRails is not built to make stablecoins exciting. It is built to make them boring enough for regulated payment operations. And in financial infrastructure, boring is the point.

Stablecoin settlement should be fast. Payment operations should be predictable. Finance should be able to reconcile. Compliance should be able to audit. Product teams should be able to launch without spending 12–24 months rebuilding infrastructure from scratch.

That is the buying reason. Not blockchain. Control.

FAQ

Why are cross-border payments still slow in 2026?

Cross-border payments are still slow because they often move across fragmented banking systems, local rails, compliance checks, FX processes, correspondent banks, and settlement windows. Even when the front-end experience looks simple, the underlying payment flow may still depend on intermediaries, cut-off times, manual reviews, and local payout constraints.

Why are cross-border payments expensive?

Cross-border payments are expensive because the visible transfer fee is only part of the total cost. Businesses may also pay through FX spreads, currency conversion markups, intermediary bank deductions, receiving bank charges, prefunded liquidity, failed payment handling, and manual reconciliation work.

How do stablecoins reduce cross-border payment costs?

Stablecoins can reduce cross-border payment costs by reducing dependency on correspondent banking, enabling faster settlement, supporting 24/7 value movement, improving liquidity mobility, and reducing the need for large prefunded balances. However, savings depend on the quality of on-ramp, off-ramp, FX, compliance, and local payout infrastructure.

What is cross-border payment infrastructure?

Cross-border payment infrastructure is the system that manages the full payment lifecycle across providers, currencies, rails, compliance checks, ledgers, reconciliation processes, and operational workflows. It is not only the rail that moves money. It is the control layer that explains, reconciles, audits, retries, and governs the movement of money.

Building cross-border payments with stablecoin rails?

Do not start with the rail, start with the operating model.

NetiRails helps fintechs, neobanks, and payment institutions launch stablecoin-based cross-border payment flows with orchestration, ledgering, compliance gates, reconciliation, provider abstraction, and auditability built in from day one.

If you are moving from idea, pilot, or provider shortlist toward production, we can help you design the flow before the provider stack becomes expensive to change.

Bring one corridor, one payment scenario, and your current provider stack. We’ll help you see where the operating risk sits before it becomes expensive to change.

.webp&w=3840&q=75)